Something a little bit unusual has been happening in Seattle this last week or two. Homes are going past their review date without offers. We have become so used to offers that waive all contingencies and escalate in price that this last week has caught all of us in the industry a bit by surprise. There are lots of conversations that are happening behind closed doors, between real estate agents. Is this the end of the crazy market? Did the head tax and looming HQ2 finally make a noticeable impact on the market? Are trade tariffs and rising interest rates putting a lid on this incredible run-up? The agents that I work with all have different opinions about what this change in the market means. Those opinions range from, the market has peaked to no, it’s just a normal June bump in inventory (June usually sees the biggest jump in properties listed for sale). It’s quite common for agents to give opinions based on their gut and their years in the business but actual data is the best way to look at this and, yes, the data show something has changed.

Low inventory, or as the MLS described it a couple of months ago, “extreme low inventory” is what causes all of the chaos in the home buying market. A normal, balanced market has about 6 months of inventory. That is, if nothing else came on the market, it would take about 6 months to sell everything that was listed. In the Seattle market we have been measuring inventory in weeks since at least 2013. Most of the time when I check inventory numbers I see two or three weeks of inventory in Seattle. If we don’t want to have crazy bidding wars for a home we simply need more homes to sell. It’s the law of supply and demand playing out in real-time and making buyers miserable and sellers ecstatic. Guess what, we suddenly have more inventory than at any time in years.

In May, we had 686 active home (houses) listings in Seattle. Compared to May of last year, that’s a 36% jump in inventory. This month’s numbers are not finalized yet but I just pulled the inventory number for today (June 16) and we have 757 homes for sale. Compared to June of 2017, that’s a 27% increase. We can speculate about what is driving this: HQ2, head tax, fed signaling 4 more interest rate hikes, 30 year fixed rate average above 4.7% already. However, getting lost in the “why” is a fun exercise but not always the most effective approach; getting solidly grounded in the data is actually instructive, and the data say that we have more inventory than we’ve had for years.

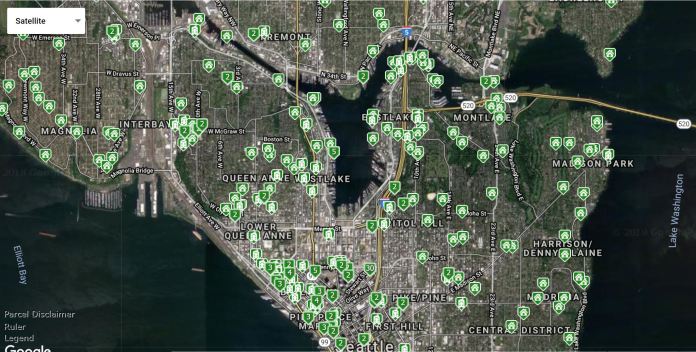

About half of my clients are investors and I want to discuss what this means for them. But for the moment let’s talk about the regular buyer, the person that needs a home to live in, raise a family in, come home to after a hard day at work. For that client, now is the time to buy. I’m usually quite reluctant to make absolute statements (and I could always be wrong) but June of 2018 is a moment-in-time in which we suddenly have more inventory than we’ve seen in years and interest rates are still very low. We also have the fact that you might be able to buy without a crazy offer that throws out all contingencies and escalates 10%, 15%, 20% or higher. To illustrate that, take a look at the map below. This shows active listings that have been on the market longer than 10 days. The significance of this is that most listings have an official review date about a week after listing, so almost all of these listings went past their review date without an offer. In theory, you should be able to buy any of these properties without competition.

There are always some listings that are problematic or overpriced but if I were to have produced that map a month ago, it would have had far fewer properties. If you are looking for a home to live in, now might be the moment to buy. Not only that, now might be the time to negotiate on price, put a full inspection contingency in-place and even negotiate up-front for seller’s concessions. I guarantee that many of the sellers on that map are feeling a little bit panicked.

If you’re an investor, I still think now is the time to buy but you definitely have to be a bit more selective. The rental market has been softening a bit for a number of months now. This is not a reversal, it’s just a slower rate of rent appreciation. I have noticed with some of my clients that they are no longer simply holding a rental open house and collecting multiple applications; instead they are showing their properties to one prospective tenant at a time. They are still renting quickly and at a good price, it’s just not as busy as it was two+ years ago. According to Zumper, Seattle is still the 8th hottest rental market in the country, but you can see from the graphic below that Seattle is holding steady but not on a hot upward or downward trend. A big factor in that is the number of new apartment buildings that have gone up in the last few years. Developers in Washington tend to build apartment buildings instead of condo buildings for a whole slew of liability issues (worthy of a separate post).

Rents have gone up a little over 4% in Seattle in the last year according to this survey. That’s fine and says to me that the rental market is healthy, although a little bit more balanced than before.

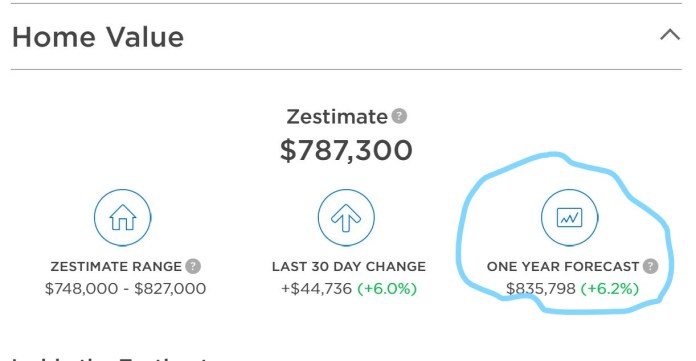

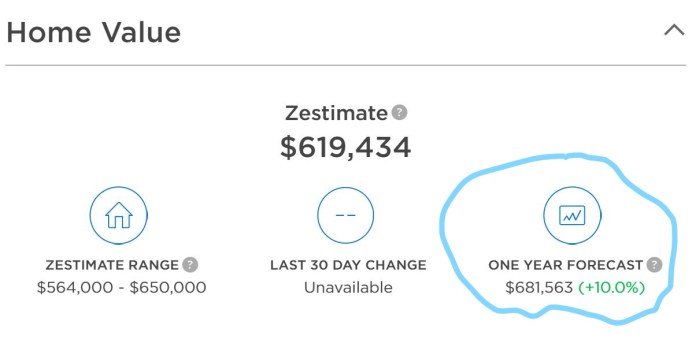

Most of my investor clients are not necessarily looking for positive cash flow from their rentals, they’re looking to have a renter make the mortgage payment and are hoping to make a return based on appreciation. If we think that all of this lessened competition and and more inventory is the end of the hot real estate market in Seattle, investors might be reluctant to invest right this moment. While I think buying a rental in 2009 or even 2016 would have been the better scenario, buying today looks pretty good as well. Most economists think this market will be hot for the foreseeable future, just not as crazy hot as it has been. Let’s take a look at some micro-level predictions for price appreciation. I like the economists at Zillow. I’ve heard their chief economist speak several times and found her to be super smart. I also think Zillow economists might pay extra close attention to Seattle since the company is based here and they probably have personal investments in the city. Here are some snapshot predictions for three neighborhoods in Seattle: Columbia City (hot neighborhood in South Seattle), Greenlake in the north and Belltown downtown. I’m pulling these from properties that I have a connection to but the individual property doesn’t matter–the predicted appreciation is for the neighborhood:

Greenlake:

Columbia City:

Belltown:

Price appreciation between 6.2% and 10% is great by almost any measure. When you also add in the fact that a tenant is going to be paying down your loan (or paying you back if you were the lender in a cash deal), you get a real return that might even be higher. It reminds me of an article that I read about Warren Buffet. He compares businesses that he is contemplating buying to the 10 year treasury rate. If we assume that a treasury note is a safe investment then the business that has risk should pay him more. Current yield on a 10 year T-bill is about 2.9%.